Cargo transportation boom of 2021

Cargo transportation boom of 2021

and why are shortages still getting worse

New report from Boeing titled Commercial Market Outlook for the period 2021–2040 paints a really rosy picture of the future of the aviation industry, with Boeing putting a lot of faith into its new wide-body airplane 7 series. That faith could be justified as widebody airplanes have a longer lifespan as they can easily be converted into medium-range freighters at the end of their life as passenger carriers.

According to the Boeing outlook report, they expect that the aviation industry will need more than 43,500 new aircraft to fulfill passengers and cargo needs valued at over $7 Trillion, that’s a trillion with a T.

Long term, market fundamentals and resilience drive demand through 2040 for more than 43,500 new airplanes valued at $7.2 trillion.

The global commercial fleet will surpass 49,000 airplanes by 2040. China, Europe, North America and other Asia-Pacific countries each account for about 20% of new airplane deliveries, with the remaining 20% going to other emerging markets.

The global freighter fleet in 2040 will be 70% larger than the pre-pandemic fleet due to sustained demand tied to expanding e-commerce and air freight's speed and reliability.

The cargo industry has always had time as a currency. The quicker you want your goods delivered the more it will cost.

Regarding the maritime shipping industry, business a booming. Overbooked, with as one person said, goods can move but it will take more money to make them move, cargo owners are right now getting the worst ever service at the absolute highest prices seen.

It’s a butterfly effect in practice, and of which we have not yet seen the end result as it will take some time for it to ripple across to the end of the supply chain.

It is sad that we allowed our railway infrastructure to fall behind as the railway is equivalent on land to cargo ships on the high seas.

At the start of the pandemic, we saw unprecedented levels of contraction in container demand. Globally speaking 15 to 20% of container demand simply just evaporated. In 2020 almost 20% of the world shipping industry was standing idle with goods were piling up at manufacturers’ warehouses or onboard ships that could not dock. But that all changed rather abruptly. Once the initial shock wore off and shipping continued problems that were piling up came to a head. The need for deliveries increased so sharply that currently there are no idle ships and freight rates also increased extremely rapidly with Maersk increased its rates by 18% during the second half of 2020.

At the same time, ports were facing problems of their own including surging demand congestion. On average ports needed to handle 30 percent more cargo through a port. Here we need to remember that it's not enough to get the containers off the ships into the port, ports are not the destination of goods. A 30% increase in traffic means that 30% more trucks are needed to drive into the port for pickup and get it to the rail or to its final destination. The fact that there is a worldwide shortage of truck drivers puts cargo ports in a difficult position as they can’t let themself be flooded with containers that just sit there. Bringing the traffic down once again to a halt. The people at the ports, the logistics people are unsung heroes. They make the world tick.

The situation will not end soon, as demand for shipping increases so does the need for end mile delivery which is in a crisis of its own. This last-mile delivery does not look that grave on the surface and to the public as they have little contact with industrial-scale delivery schedules or needs. Most of the public is served with new delivery services that share their business models with Uber or an ownerless business. A business that doesn’t own the means of fulfillment but acts as an intermediator between a person with a need and a person that agreed to deliver the goods.

As for Boeing and their biggest projected market is Aisa-Pacific with 17,645 planes in the next 20 years or 40% of the total. From which China is responsible for 75% of that or around 13 thousand planes.

With the situation in the world as it currently stands at the tail end of 2021 that outlook is optimistic. More and more companies are opting for local production and companies are leaving China. Among others before, this month Samsung heavy Industries, Japanese electronics giant Toshiba and Swedish telecom manufacturer Ericsson have closed their branches in China. Coupled with the coming down of real a state Godzilla Evergrande. These are truly interesting times for China.

On the political side, Boeing could find itself behind a sanction wall with china. This could make the Chinese government look inward and shift its resources toward COMAC or the Commercial Aircraft Corporation of China for their airplane needs, and cutting ties from western manufacturers.

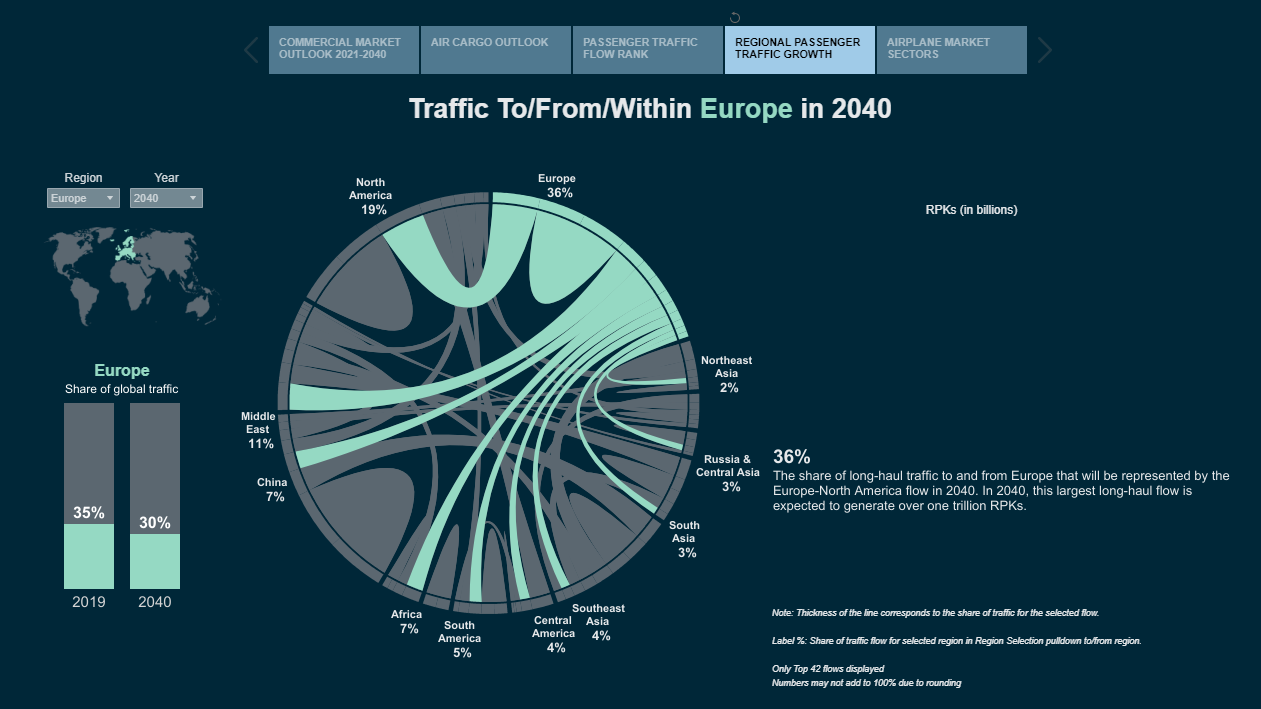

Further down in the report there’s a 20-year projection from Boing per region. It shows us how the world is connected.

The shipping industry could really benefit from AI-assisted controlled ships as stated in “Annual Overview of Marine Casualties and Incidents 2018” published by the European Maritime Safety Agency, 57.8% of accidents were attributable to human factors, illustrating a similar trend in other parts of the world. Some are already looking in that direction with Nippon Foundation's report entitled, "Future 2040 — The Future of Japan Created by Unmanned ships", issued in April 2019, is assuming that ships to be newly built in 2040 are mainly expected to be unmanned and that 50% of domestic ships will be unmanned, the economic effect of unmanned ships is estimated at approximately ¥1 trillion or around $9 billion in 2040.